A DEEPER LOOK AT MARKET CORRECTIONS

While market corrections occur on a regular basis—and should be expected—staying invested amid the volatility can prove challenging for even the most seasoned investors.

It’s hard to believe, but this week marks the 11 year anniversary from the stock market bottom made on March 9, 2009. And since that bottom, markets have rallied for the past 11 years, racking up a total return (inclusive of dividends) of more than 450%. Yes, 450%. That works out to a 16.8% annualized return. But in a couple short weeks, equity markets have declined nearly 20% from their record highs. And not only have the declines been substantial, the pace at which they occurred was extremely rapid. Fears surrounding coronavirus (COVID-19) and the oil price war between Russia and Saudi Arabia have caused a ripple effect throughout the markets.

WHAT IS A MARKET CORRECTION AND HOW COMMON ARE THEY?

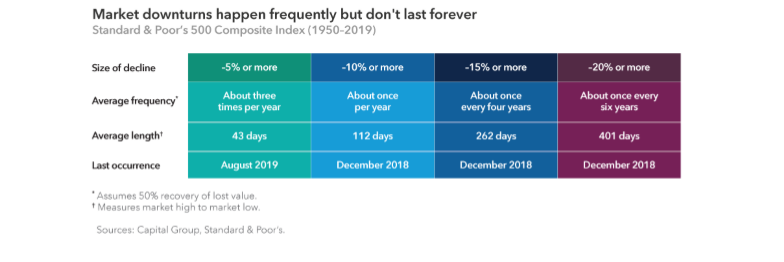

Pullbacks, corrections, bear markets, and downturns—call it what you will, but it all translates to a decline in value of the stock market. Generally speaking, we categorize a pullback as roughly a 5% decline, a correction being 10%, while a bear market tends to be 20% or more. And while they never feel good, we should be used to them as they occur regularly—albeit for different reasons (in this case, coronavirus). The chart below, courtesy of my friends at Capital Group (parent of American Funds), highlights the frequency with which declines tend to occur.

BUT WAIT, IS THIS TIME DIFFERENT? IT FEELS DIFFERENT…

Having advised clients during the 2008-2009 financial crisis, Brexit, the 2010 “flash crash,” the debt ceiling crisis, yield curve inversions, trade wars and tariffs, hurricanes, and more—I’ve experienced first-hand both the apparent fragility of the markets, but also the overwhelming resiliency of the markets. There’s no doubt that the fast-paced movement of the market can distract us, but we must remember that at the end of the day, when we invest, we’re really making an investment in our future. By investing, we are putting faith that the world will go on, people will continue to go to school, to work, they will invent products, services, and cures, and I believe that’s why this time is no different. The current events we’re facing are serious, and they will have implications to be sure, but history tells us that we’ve been through this before. I strongly suspect that when we look back one, two, five, or ten years from now, we will have recalled how challenging this period was, but that we’ll be glad we did not abandon a well-constructed investment strategy. The chart of the S&P 500 index below highlights that we’ve experienced these types of declines on a fairly regular basis. Do you remember late 2018 when the markets were down during the year, almost as much as they are down today? Thankfully, most investors stayed the course and just a few weeks later—in 2019— enjoyed some of the strongest returns in market history.

WHEN WILL THE VOLATILITY END? AND WILL WE FALL INTO A RECESSION?

One of the hardest parts of successful investing is that you must keep faith and courage. If we knew when markets would turn higher or lower, there would be no returns to be had—because there would be no risk. I believe it’s also important to note that virtually no one saw this market decline coming. And just as no one forecasted this decline, I truly doubt that anyone will be able to predict when it will end (shy of a lucky guess). So if we can’t predict, we ought to prepare. I’ve told investors for years that if you need funds in the short term, they shouldn’t be in the market. And this is why. But for longer-term dollars, the events of today should be of little concern.

You’re also hearing rumors of a possible recession. And to be frank, it is possible—because it’s always possible. However, going into March of this year, the U.S. economy was in strong shape with low unemployment, low inflation, an increasing level of personal savings, and a historically low household debt-to-disposable income ratio. I suspect this relative strength will help soften the negative impact from the coronavirus and oil price wars. We also know that the Federal Reserve—along with other central banks around the world— has actively sought to loosen monetary policy as a tool to stave off a recession. So will we fall into recession? I don’t know. And no one can say for sure. But if you’re investing appropriately for your individual objectives, you should keep faith in your planning efforts and focus on what you can control.

ACTION ITEMS FOR INVESTORS IN THE CURRENT ENVIRONMENT

I’ll conclude by offering a few potential action items as you persevere through this period of heightened market volatility:

• Review your financial plan. For most who have planned ahead, they’ve tested their approach for events like these

• Review your portfolio allocation and if it’s no longer aligned with your stated tolerances, consider adjusting

• If you have short-term dollars invested in the market, consider pulling them as we could see further declines

• If your invested dollars are for a goal more than 5 years into the future, I urge you to keep a cool head and avoid trying to outsmart the market by timing or trading

• Evaluate if this is an appropriate time to convert part of your IRA to a Roth IRA while values are down

• Seek opportunities to harvest losses in taxable accounts

CLOSING NOTE

One of my personal goals is always try and get a little better at everything I do. When it comes to investing, I try to learn lessons from others and also from my own past experiences. One lesson I’ve learned is that, often after we’ve experienced previous declines (and subsequent recoveries) clients tell me they wish they had the courage to invest more dollars when prices were lower. Only you can decide if you have the fortitude to do this, but if history is any guide, you may be well-rewarded for taking risk when others chose to panic.

As always, I’m here if you have any questions or if you would like to discuss your personal situation.

Sincerely,

Jeff DeLarme, CFP®

Registered Principal, Financial Advisor

Disclosures

Please note, changes in tax laws or regulations may occur at any time and could substantially impact your situation. While familiar with the tax provisions of the issues presented herein, Raymond James financial advisors are not qualified to render advice on tax or legal matters. You should discuss any tax or legal matters with the appropriate professional. The information in this writing has been prepared from sources believed to be reliable, but is not guaranteed by Raymond James Financial Services or DeLarme Wealth Management and is not a complete summary or statement of all available data necessary for making an investment decision. Any information provided is for informational purposes only and does not constitute a recommendation.

Capital Group and American Funds are not affiliated with Raymond James or DeLarme Wealth Management, Inc.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. Any opinions are those of Jeff DeLarme and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual performance. Individual investor’s results will vary. Past performance does not guarantee future results. Future investment performance cannot be guaranteed, investment yields will fluctuate with market conditions.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. DeLarme Wealth Management is not a registered broker/dealer, and is independent of Raymond James Financial Services.